Startup-focused lender SVB Financial Group became the largest bank failure since the financial crisis on Friday, in a sudden collapse that roiled global markets and stranded billions of dollars belonging to companies and investors.

California banking regulators closed the bank, which did business as Silicon Valley Bank, on Friday and appointed the Federal Deposit Insurance Corporation (FDIC) as receiver for later disposition of its assets.

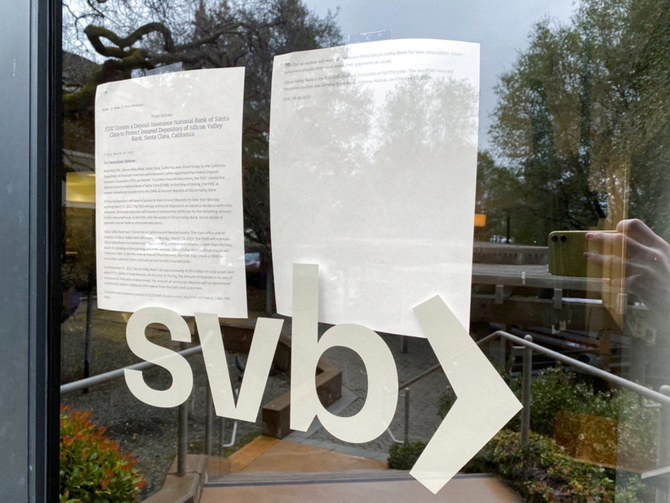

The main office and all branches of Silicon Valley Bank will reopen on March 13 and all insured depositors will have full access to their insured deposits no later than Monday morning, the FDIC said.

But 89 percent of the bank’s $175 billion in deposits were uninsured as the end of 2022, according to the FDIC, and their fate remains to be determined.

Companies such as video game maker Roblox Corp. and streaming device maker Roku Inc. said they had hundreds of millions of deposits at the bank. Roku said its deposits with SVB were largely uninsured, sending its shares down 10 percent in extended trading.

Technology workers whose paychecks relied on the bank were also worried about getting their wages on Friday. An SVB branch in San Francisco showed a note taped to the door telling clients to call a toll-free telephone number.

The FDIC said it would seek to sell SVB’s assets and that future dividend payments may be made to uninsured depositors.

At times in the past, the FDIC has moved quickly, even striking deals to sell major banks over the weekend.

SVB did not respond to calls for comment.

The collapse sent shockwaves through the startup community, which has come to view the lender as a source of reliable capital.

The bank’s customers were met with locked doors on Friday. A client dashboard was down, a UK-based client of the bank told Reuters.

Dean Nelson, CEO of Cato Digital, was on a line outside of SVB Santa Clara headquarters, hoping to get answers. Nelson said he was worried about the company’s ability to pay employees and cover expenses.

“Access to the cash is the biggest problem for the majority of the companies here. If you’re a startup, cash is king. The cash and the workflow, to be able to have the runway is critical.”

The problems at SVB, which quickly escalated after the bank said on Wednesday it would raise money, underscore how a campaign by the US Federal Reserve and other central banks to fight inflation by ending the era of cheap money is exposing vulnerabilities in the market. The worries walloped the banking sector.

US banks have lost over $100 billion in stock market value over the past two days, with European banks losing around another $50 billion in value, according to a Reuters calculation. Regional banks sold off on Friday.

US lenders First Republic Bank and Western Alliance said on Friday their liquidity and deposits remained strong, aiming to calm investors as their shares fell. Others such as Germany’s Commerzbank issued unusual statements to reassure investors.

Some analysts forecast more pain for the sector as the episode spread concern about hidden risks in the banking sector and its vulnerability to the rising cost of money.

“There could be a bloodbath next week as banks are in trouble, the short sellers are out there and they are going to attack every single bank, especially the smaller ones,” said Christopher Whalen, chairman of Whalen Global Advisers.

US Treasury Secretary Janet Yellen met with banking regulators on Friday expressed “full confidence” in their abilities to respond to the situation, Treasury said.

The White House on Friday said it had faith and confidence in US financial regulators, when asked about the failure of SVB. Cecilia Rouse, who chairs the Council of Economic Advisers, said the US banking system was fundamentally stronger than it was during the 2008 financial crisis.

“The first bank failure since 2020 is a wake-up call,” said Matthew Goldberg, an analyst at Bankrate.

The genesis of SVB’s collapse lies in a rising interest rate environment. As higher interest rates caused the market for initial public offerings to shut down for many startups and made private fundraising more costly, some SVB clients started pulling money out.

To fund the redemptions, SVB sold on Wednesday a $21 billion bond portfolio consisting mostly of US Treasuries, and said it would sell $2.25 billion in common equity and preferred convertible stock to fill its funding hole.

Its stock collapsed and depositors started to panic. SVB scrambled this week to reassure its venture capital clients their money was safe. By Friday, the collapsing stock price had made its capital raise untenable and sources said the bank tried to look at other options, including a sale, until regulators stepped in and shut the bank down.

After the FDIC announcement, employees received an email from the company saying they would be contacted by officials about employment and compensation, according to a source who declined be identified. As of Friday evening, there had not been any further communication from the company or the FDIC, the source said.

The last FDIC-insured institution to close was Almena State Bank in Kansas, on October 23, 2020.