NEW DELHI/MUMBAI: Adani’s market losses swelled above $100 billion on Thursday, sparking worries about a potential systemic impact a day after the Indian group’s flagship firm abandoned its $2.5 billion stock offering.

Another challenge for Adani on Thursday came when S&P Dow Jones Indices said it would remove Adani Enterprises from widely used sustainability indices, effective Feb. 7, which would make the shares less appealing to sustainability-minded funds.

In addition, India’s National Stock Exchange said it has placed on additional surveillance shares of Adani Enterprises , Adani Ports and Ambuja Cements .

However, Adani Group Chairman Gautam Adani is in talks with lenders to prepay and release pledged shares as he seeks to restore confidence in the financial health of his conglomerate, Bloomberg News reported on Thursday.

The shock withdrawal of Adani Enterprises’ share sale marks a dramatic setback for founder Adani, the school dropout-turned-billionaire whose fortunes rose rapidly in recent years but have plunged in just a week after a critical research report by US-based short-seller Hindenburg Research.

ALSO READ: Who is Hindenburg, the firm targeting India’s Adani?

Aborting the share sale sent shockwaves across markets, politics and business. Adani stocks plunged, opposition lawmakers called for a wider probe and India’s central bank sprang into action to check on the exposure of banks to the group. Meanwhile, Citigroup’s wealth unit stopped making margin loans to clients against Adani Group securities.

The crisis marks an dramatic turn of fortune for Adani, who has in recent years forged partnerships with foreign giants such as France’s TotalEnergies and attracted investors such as Abu Dhabi’s International Holding Company as he pursues a global expansion stretching from ports to the power sector.

In a shock move late on Wednesday, Adani called off the share sale as a stocks rout sparked by Hindenburg’s criticisms intensified, despite it being fully subscribed a day earlier.

“Adani may have started a confidence crisis in Indian shares and that could have broader market implications,” said Ipek Ozkardeskaya, senior market analyst at Swissquote Bank.

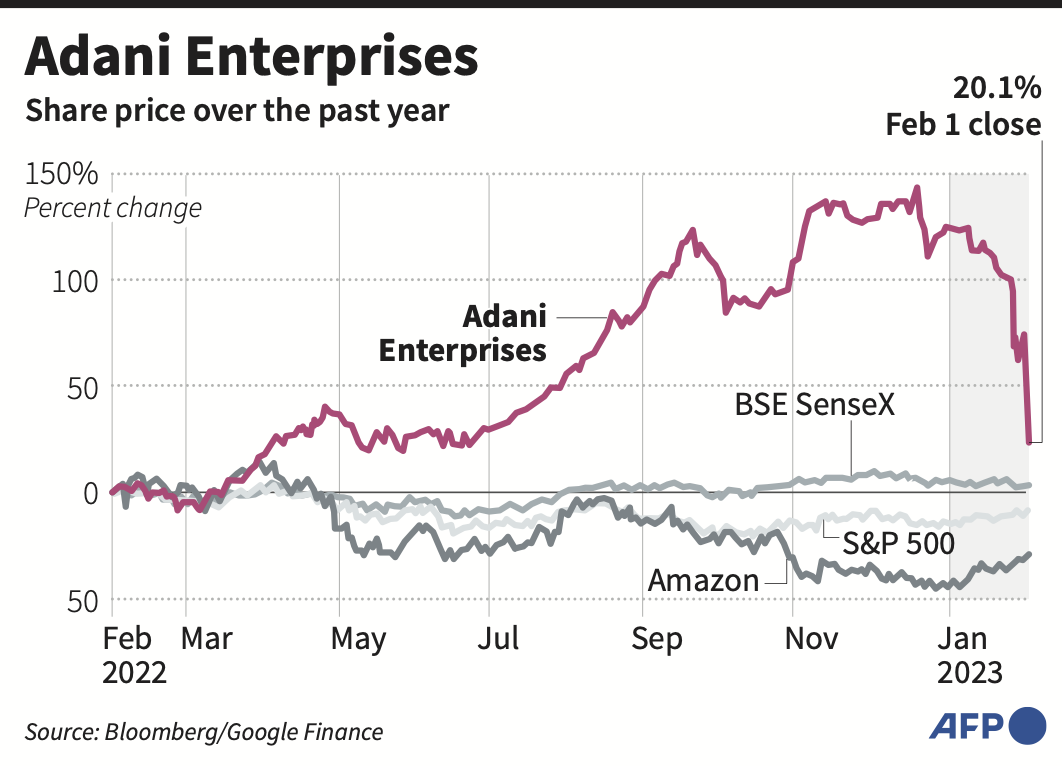

Adani Enterprises shares tumbled 27 percent on Thursday, closing at their lowest level since March 2022.

Other group companies also lost further ground, with 10 percent losses at Adani Total Gas, Adani Green Energy and Adani Transmission, while Adani Ports and Special Economic Zone shed nearly 7 percent.

Since Hindenburg’s report on Jan. 24, group companies have lost nearly half their combined market value. Adani Enterprises — described as an incubator of Adani’s businesses — has lost $26 billion in market capitalization.

Adani is also no longer Asia’s richest person, having slid to 16th in the Forbes rankings of the world’s wealthiest people, with his net worth almost halved to $64.6 billion in a week.

The 60-year-old had been third on the list, behind billionaires Elon Musk and Bernard Arnault.

His rival Mukesh Ambani of Reliance Industries is now Asia’s richest person.

Mukesh Ambani, chairman oil-to-telecom conglomerate Reliance Industries, is now Asia''s richest person. (AFP) file)

Broader concerns

Adani’s plummeting stock and bond prices have raised concerns about the likelihood of a wider impact on India’s financial system.

India’s central bank has asked local banks for details of their exposure to the Adani Group, government and banking sources told Reuters on Thursday.

CLSA estimates that Indian banks were exposed to about 40 percent of the $24.5 billion of Adani Group debt in the fiscal year to March 2022.

Dollar bonds issued by entities of Adani Group extended losses on Thursday, with notes of Adani Green Energy crashing to a record low. Adani Group entities made scheduled coupon payments on outstanding US dollar-denominated bonds on Thursday, Reuters reported citing sources.

“We see the market is losing confidence on how to gauge where the bottom can be and although there will be short-covering rebounds, we expect more fundamental downside risks given more private banks (are) likely to cut or reduce margin,” said Monica Hsiao, chief investment officer of Hong Kong-based credit fund Triada Capital.

In New Delhi, opposition lawmakers submitted notices in parliament demanding discussion of the short-seller’s report.

The Congress Party called for a Joint Parliamentary Committee be set up or a Supreme Court monitored investigation, while some lawmakers shouted anti-Adani slogans inside parliament, which was adjourned for the day.

Adani vs Hindenburg

Adani made acquisitions worth $13.8 billion in 2022, Dealogic data showed, its highest ever and more than double the previous year.

The canceled fundraising was critical for Adani, which had said it would use $1.33 billion to fund green hydrogen projects, airports facilities and greenfield expressways, and $508 million to repay debt at some units.

Hindenburg’s report alleged an improper use of offshore tax havens and stock manipulation by the Adani Group. It also raised concerns about high debt and the valuations of seven listed Adani companies.

The Adani Group has denied the accusations, saying the allegation of stock manipulation had “no basis” and stemmed from an ignorance of Indian law. It said it has always made the necessary regulatory disclosures.

Adani had managed to secure share sale subscriptions on Tuesday even though the stock’s market price was below the issue’s offer price. Maybank Securities and Abu Dhabi Investment Authority had bid for the anchor portion of the issue, investments which will now be reimbursed by Adani.

Late on Wednesday, the group’s founder said he was withdrawing the sale given the share price fall, adding his board felt going ahead with it “will not be morally correct.”