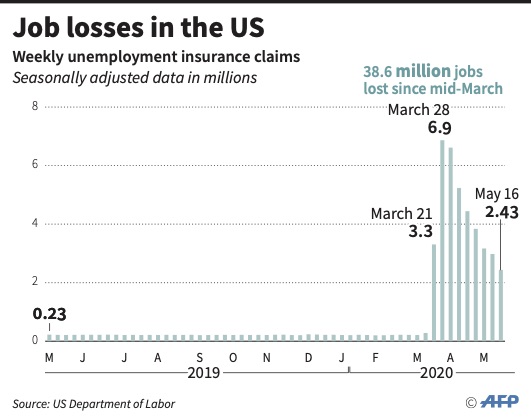

WASHINGTON: The number of Americans applying for unemployment benefits in the two months since the coronavirus took hold in the US has swelled to nearly 39 million, the government reported Thursday, even as states from coast to coast gradually reopen their economies and let people go back to work.

More than 2.4 million people filed for unemployment last week in the latest wave of layoffs from the business shutdowns that have brought the economy to its knees, the Labor Department said.

That brings the running total to a staggering 38.6 million, a job-market collapse unprecedented in its speed.

The number of weekly applications has slowed for seven straight weeks. Yet the figures remain breathtakingly high — 10 times higher than normal before the crisis struck.

And the continuing rise shows that even though all states have begun reopening over the past three weeks, employment has yet to snap back and the outbreak is still damaging businesses and destroying jobs.

“While the steady decline in claims is good news, the labor market is still in terrible shape,” said Gus Faucher, chief economist at PNC Financial.

Federal Reserve Chairman Jerome Powell said over the weekend that US unemployment could peak in May or June at 20% to 25%, a level last seen during the depths of the Great Depression almost 90 years ago. Unemployment in April stood at 14.7%, a figure also unmatched since the 1930s.

Over 5 million people worldwide have been confirmed infected by the virus, and about 330,000 deaths have been recorded, including more than 93,000 in the US and around 165,000 in Europe, according to a tally kept by Johns Hopkins University and based on government data. Experts believe the true toll is significantly higher.

In other developments:

• President Donald Trump’s approval ratings have remained steady amid the crisis, underscoring the way Americans seem to have made up their minds about him. A poll from The Associated Press-NORC Center for Public Affairs Research found that 41% approve of his job performance, while 58% disapprove. That’s consistent with opinions of him throughout his three years in office.

•Trump made a trip to Michigan to tour a Ford factory that has been retooled to manufacture ventilators, and he did not wear a face covering despite a warning from the state’s top law enforcement officer that a refusal might lead to a ban on his return. The president has been locked in a feud with the state’s Democratic governor over the outbreak and has also threatened to withhold federal funds over Michigan’s expansion of voting by mail.

Across the US, some companies have begun to rehire their laid-off employees as states have eased restrictions on movement and commerce. On Monday, more than 130,000 workers at the three major American automakers, plus Toyota and Honda, returned to their factories for the first time in two months.

Still, major employers continue to cut jobs. Uber said this week that it will lay off 3,000 more employees because demand for rides has plummeted. Digital publishers Vice, Quartz and BuzzFeed, magazine giant Conde Nast and the owner of The Economist magazine announced job cuts last week.

Stephen Stanley, chief economist at Amherst Pierpont, said the latest layoffs may be particularly worrisome because they are happening even as states reopen. That could mean many companies see little hope of a substantial economic recovery anytime soon and still feel a need to cut jobs.

“There’s a high probability that those layoffs could persist for longer than those that were a function of (businesses) just being closed,” Stanley said.

The latest figures do not mean 38.6 million people are out of work. Some have been called back, and others have landed new jobs. But the vast majority are still unemployed.

An additional 1.2 million people applied for unemployment last week under a federal program that makes self-employed, contractor and gig workers eligible for the first time. But those figures aren’t adjusted for seasonal variations, so the government doesn’t include them in the overall number of applications.

One rehired worker, Norman Boughman, received an email last week from his boss at a second-hand clothing store in Richmond, Virginia, where he worked part time, asking him to return. But even with a mask, he worries about his health.

“We’re having to sort through people’s things, and I feel like that puts us at a higher risk,” he said.

European countries have also seen heavy job losses, but robust government safety-net programs in places like German and France are subsidizing the wages of millions of workers and keeping them on the payroll.

Another 2.43 million US workers were put out of work last week amid the coronavirus pandemic, according to government data released on May 21, 2020, bringing the total since mid-March to a massive 38.6 million. (AFP / Olivier Douliery)

Meanwhile, doubts are growing over ambitious plans by European governments to use contact-tracing smartphone apps to fight the spread of the virus as they ease their lockdowns. The apps can help authorities determine whether people have crossed paths with those who are infected.

British Security Minister James Brokenshire told the BBC that an app that was supposed to be introduced by mid-May is not ready, suggesting “technical issues” were to blame. Similarly, France delayed last week’s roll-out of its app because of technical problems and privacy concerns.

Italy’s premier said testing of his country’s app will begin in the coming days, and Spain plans to try out its technology at the end of June in the Canary Islands.

As for the search for a vaccine, drug maker AstraZeneca said it has secured agreements to produce 400 million doses of a still experimental and unproven formulation that is being tested at the University of Oxford. It is one of the most advanced projects in the international race for a vaccine.

While no vaccine has yet been proven to work against the virus, companies and governments are already working to crank out some of the more promising candidates in hopes of saving time. It is a big gamble that could result in millions of doses being thrown out if the potential vaccine doesn’t pan out.

AstraZeneca said it has received more than $1 billion from a US government research agency for the development, production and delivery of the vaccine.

Around the world, the effort to get back to business is raising worries over the risk of new infections, from hard-hit Milan, Italy, to meatpacking plants in Colorado and garment factories in Bangladesh.

In China, the communist leadership took extensive precautions as it prepared for the opening of its long-postponed National People’s Congress on Friday in Beijing. An outbreak there could be a public relations nightmare as President Xi Jinping showcases China’s apparent success in curbing the virus that first emerged in Wuhan late last year.