Muhammad Ali’s refusal to sign his Vietnam-era military draft card upended the boxing champ’s life and added a powerful voice to the anti-war movement. Now that piece of history is coming up for sale.

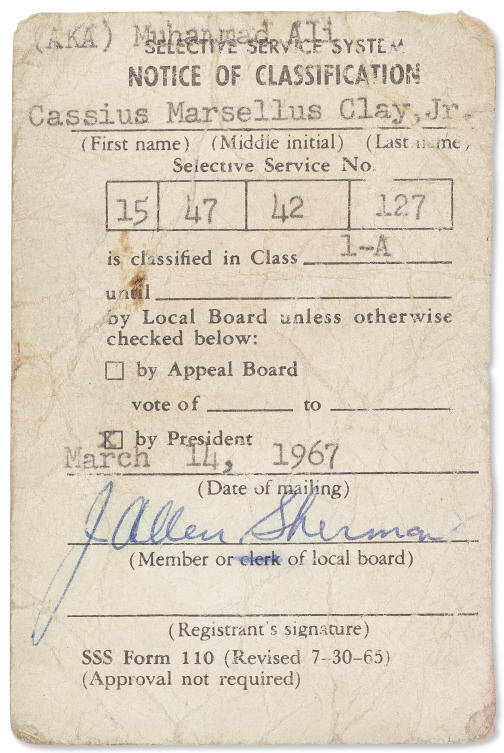

There’s a blank line on the card where Ali was supposed to sign in 1967 but refused to do so — a polarizing act of defiance as the Vietnam War raged on. It triggered a chain of events that disrupted his storied boxing career but immortalized him outside the ring as a champion for peace and social justice.

“Being reminded of my father’s message of courage and conviction is more important now than ever, and the sale of his draft card at Christie’s is a powerful way to share that legacy with the world,” Rasheda Ali Walsh, a daughter of Ali, said Thursday in a statement issued by the auction house.

The auction house said it will hold the online sale Oct. 10-28, adding the card came to it via descendants of Ali. A public display of the card began Thursday at Rockefeller Center in New York and will continue until Oct. 21. The document could fetch $3 million to $5 million, Christie’s estimated.

“This is a singular object associated with an important historical event that looms large in our shared popular culture,” said Peter Klarnet, a Christie’s senior specialist.

Ali, the three-time heavyweight boxing champion, died in 2016 at age 74 after a long battle with Parkinson’s disease. An estimated 100,000 people chanting, “Ali! Ali!” lined the streets of his hometown of Louisville, Kentucky, as a hearse carried his casket to a local cemetery. His memorial service was packed with celebrities, athletes and politicians.

The draft card, typewritten in parts, conjures memories from when Ali wasn’t universally beloved but instead stood as a polarizing figure, revered by millions worldwide and reviled by many.

For refusing induction into the US Army, Ali was convicted of draft evasion, stripped of his boxing title and banned from boxing. Ali appealed the conviction on grounds he was a Muslim minister. He famously proclaimed: “I ain’t got no quarrel with them Viet Cong.”

During his banishment, Ali spoke at colleges and briefly appeared in a Broadway musical. He was allowed to resume boxing three years later.

He was still facing a possible prison sentence when in 1971 he fought Joe Frazier, his archrival, for the first time in what was labeled “The Fight of the Century.” A few months later the US Supreme Court overturned the conviction on an 8-0 vote.

The draft card was issued the day the draft board in Louisville ordered Ali to appear for induction, Christie’s said Thursday in a news release. The card was signed by the local draft board chairman but pointedly not by Ali.

The card identified him by his birth name — Cassius Marcellus Clay Jr. — but misspelled his given middle name. Upon his conversion to Islam, he was given a name reflecting his faith, the Muhammad Ali Center in Louisville says on its website. Meanwhile, the top of the draft card reads: “(AKA) Muhammad Ali.”

The Ali Center features exhibits paying tribute to Ali’s immense boxing skills. But its main mission, it says, is to preserve his humanitarian legacy and promote his six core principles: spirituality, giving, conviction, confidence, respect and dedication.

Now an artifact reflecting how Ali personified some of those principles will be up for auction.

“This is the first time collectors will be able to acquire a vital and intimate document connected to one of the most important figures of the last century,” Klarnet said Thursday.

![]()

![]()

![]()

Muhammad Ali’s unsigned draft card, a piece of Vietnam-era history, will be auctioned

Short Url

https://arab.news/n257d

Muhammad Ali’s unsigned draft card, a piece of Vietnam-era history, will be auctioned

- There’s a blank line on the card where Ali was supposed to sign in 1967 but refused to do so

- The document could fetch $3 million to $5 million, the auction house estimated

Latest updates

Recommended

© 2026 SAUDI RESEARCH & PUBLISHING COMPANY, All Rights Reserved And subject to Terms of Use Agreement.