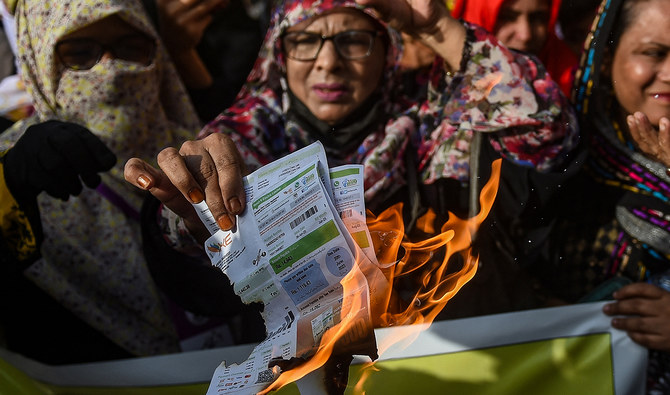

ISLAMABAD: The chief of Pakistani religious-political party, the Jamaat-e-Islami (JI), said on Monday it would hold a sit-in in Islamabad on July 12 to exert pressure on the federal government to lower taxes and reduce electricity bills.

Pakistan’s tax-heavy $67.76 billion budget for the new fiscal year came into effect today, Monday, amid an annual inflation projection of up to 13.5 percent for June.

The ambitious budget with a challenging tax revenue target of Rs13 trillion ($46.66 billion) has drawn the ire of the government’s allies and opposition alike. The revenue collection target for the new fiscal year is almost 40 percent higher than the last fiscal year. The last five months have also seen steep increases in electricity and gas bills of consumers and industries.

“Today, a joint meeting of party representatives from all over the country was conducted and we decided to hold a large dharna in Islamabad on July 12,” the JI party chief Hafiz Naeem-ur-Rehman said on Monday at a press conference in the southern port city of Karachi, the country’s commercial hub. “The sit-in will be held to lower taxes and also the per unit value of electricity.”

Lamenting the increase in the new budget on the tax liability of the salaried class, Rehman said many working professionals, including doctors, engineers and chartered accountants, were leaving Pakistan due to the unfair policies.

“Everybody is trying to get out of Pakistan due to inflation, unemployment and increased taxes,” the JI chief said.

The rise in the Pakistan government’s tax target is made up of a 48 percent increase in direct taxes and a 35 percent hike in indirect taxes over revised estimates of the current year. Non-tax revenue, including petroleum levies, is seen increasing by 64 percent. The tax would increase to 18 percent on textile and leather products as well as mobile phones besides a hike in the tax on capital gains from real estate. Workers will also get hit with more direct tax on income.

Opposition parties, mainly parliamentarians backed by the jailed former Prime Minister Imran Khan, and major trade bodies have rejected the budget, saying it will be highly inflationary and lead to industry shutdowns.