What happened:

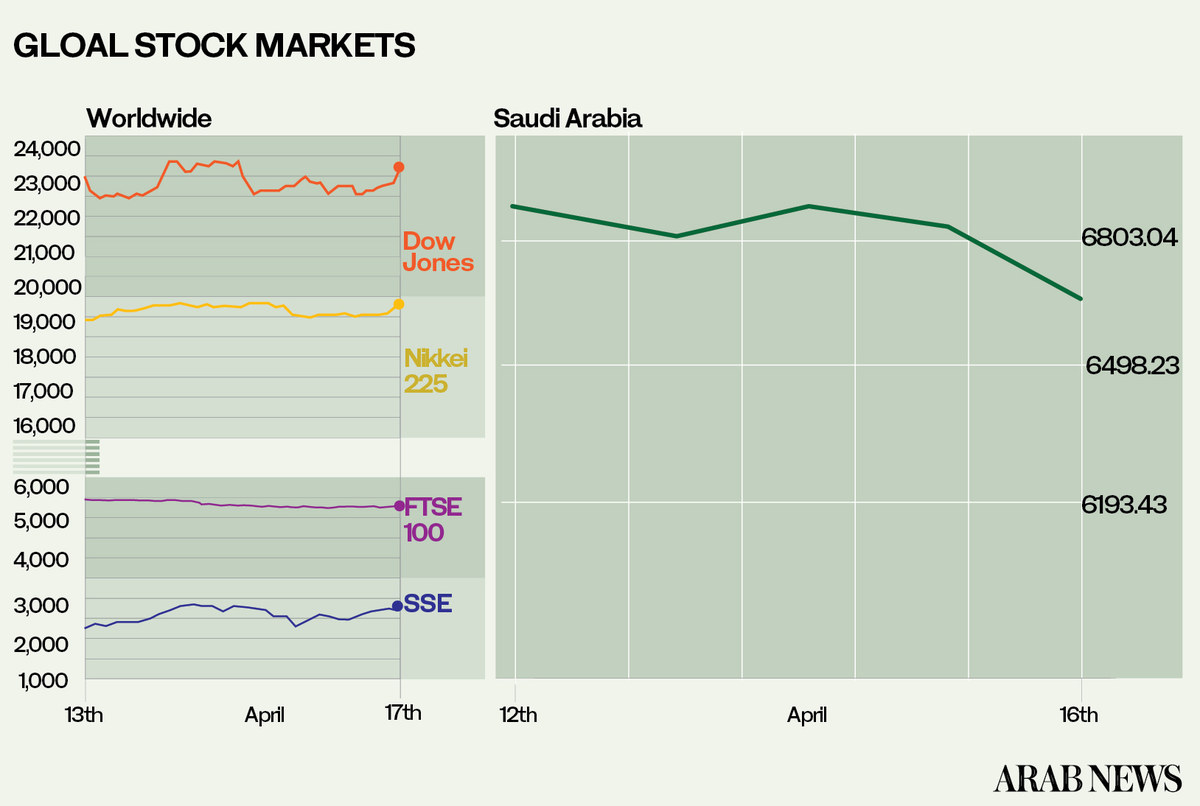

Major markets were up last week amid high volatility. It was the start of the earnings season, where Q1 results reflected the last quarter before the lockdown really hit Europe and the US.

There was a trend against emphasis on guidance, because of a lack of visibility on the full impact of the second quarter and inability to forecast the shape and pace of recovery as economies emerge from lockdown. Banks all shored up their loan loss provisions in expectation of a deterioration of their loan portfolios.

The President of the Cleveland Federal Reserve Bank, Loretta Mester, warned against the risk-on sentiment becoming too buoyant because the crisis was still ongoing and the shape and speed of any recovery unknown. She has a point. Several economists calculated that leaving major economies in lockdown could cost their gross domestic products 3 percentage points per month.

Mester explained the Fed’s interventions as a) ensuring a continued functioning of markets via the asset purchase program and b) mitigating the effects of the crisis on households and businesses by ensuring credit flows to them. They are inherently linked because functioning markets are the transmission mechanism enabling credit to flow.

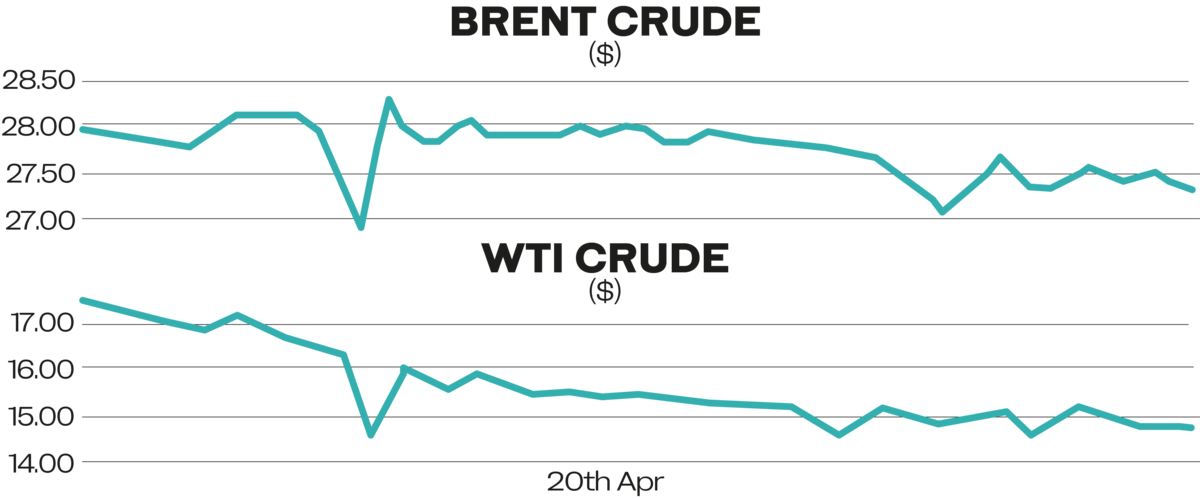

Oil had a very bad start of the week with Brent having lost 6.8 percent on the day and WTI’s May forward contract at $11.05 down 39.52 percent on the day by mid-afternoon in Europe. The June contract is considerably higher.

The Bank of Spain forecast that Spain’s economy would contract between 6.8 and 12.4 percent in 2020.

Background:

The fall in the oil price reflects the world running out of storage capacity. The differential between Brent and WTI reflects the situation in the US. Some producers sell their crude at $2 per barrel. It is not beyond the imagination that producers must have to pay off-takers if the situation does not improve.

The OPEC+ deal, which takes 9.7 million barrels out of the market, only kicks in on May 1 and mostly affects Asia and Europe. It cannot compensate for the dramatic demand in decline which the International Energy Agency forecasts to stand at 23 million barrels per day during the second quarter. What it will do, however, is flatten the curve and extend the ability of stage facilities to take in crude.

We should not forget that what happens in the US shale space has big ramifications for some US lenders, if they are exposed to the traditionally highly leveraged producers in the shale space. This, and the effects the situation has on employment, explains why US President Donald Trump’s administration is considering paying oil companies to leave crude in the ground.

Going forward:

The chilling numbers out of Spain on Monday morning highlight the problems faced by the EU. Both Spain and Italy fail the loan/GDP criteria by far. Italy’s debt to GDP ratio may reach anywhere between 150 and 180 percent at the end of the crisis.

It brings to the fore how the EU will deal with the economic fallout of the coronavirus crisis. There is the problem of mutualization of debt in the eurozone which France, Spain, Italy and other southern countries favor and their northern counterparts like Germany and the Netherlands oppose.

One way around the problem could be to permit the EU Commission borrowing to fund an investment-led recovery plan under the Multiannual Financial Framework, the EU’s seven-year budget. This plan is still on the drawing board.

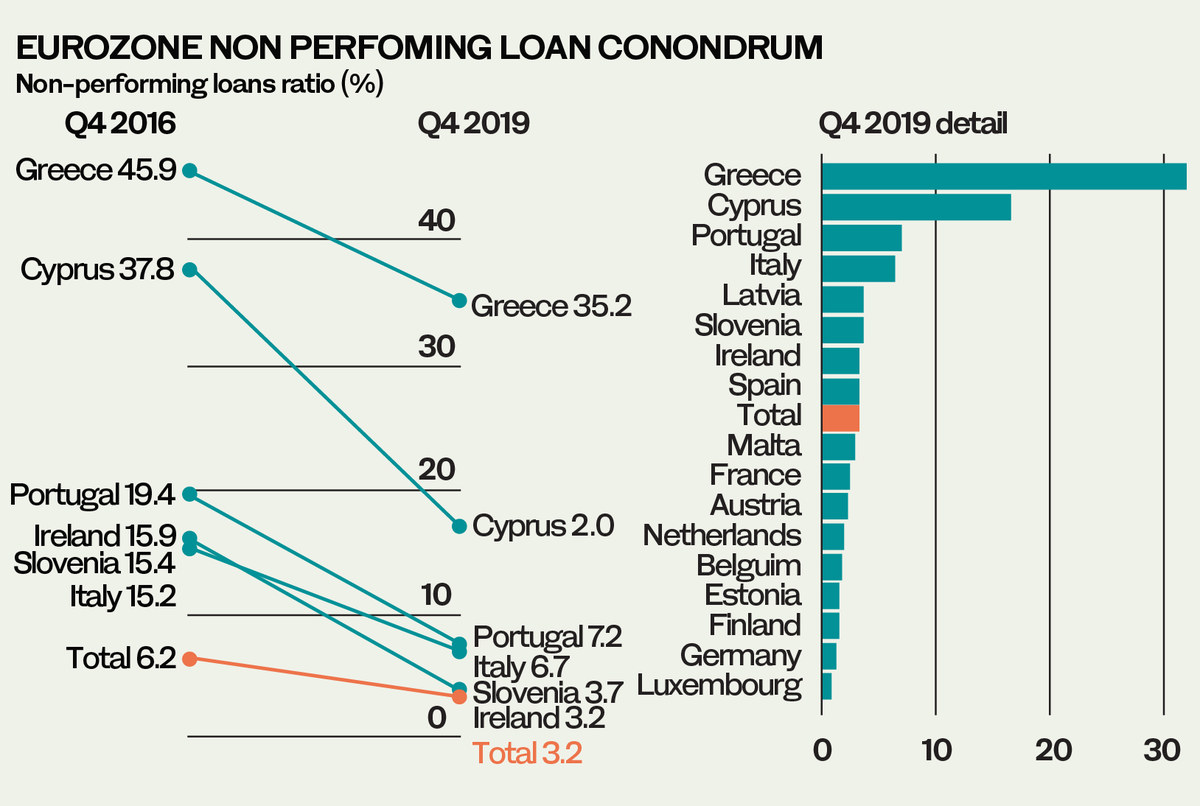

In the meantime, there is the non-performing loan (NPL) legacy of the 2008 financial crisis, leaving many eurozone countries with a mountain of NPLs. According to the Financial Times, the ECB is considering creating a “bad bank” to avoid NPLs clogging up the lending capacity of its banks, giving them headroom to lend as Europe emerges from the coronavirus-induced lockdown. This proposal is also still on the drawing board and there is no decision structure about the “bad bank” — national versus eurozone-wide — as of yet. However, it is crucial to find a solution to the NPL issue in order to support any recovery.

— Cornelia Meyer is a Ph.D.-level economist with 30 years of experience in investment banking and industry. She is chairperson and CEO of business consultancy Meyer Resources.

Twitter: @MeyerResources