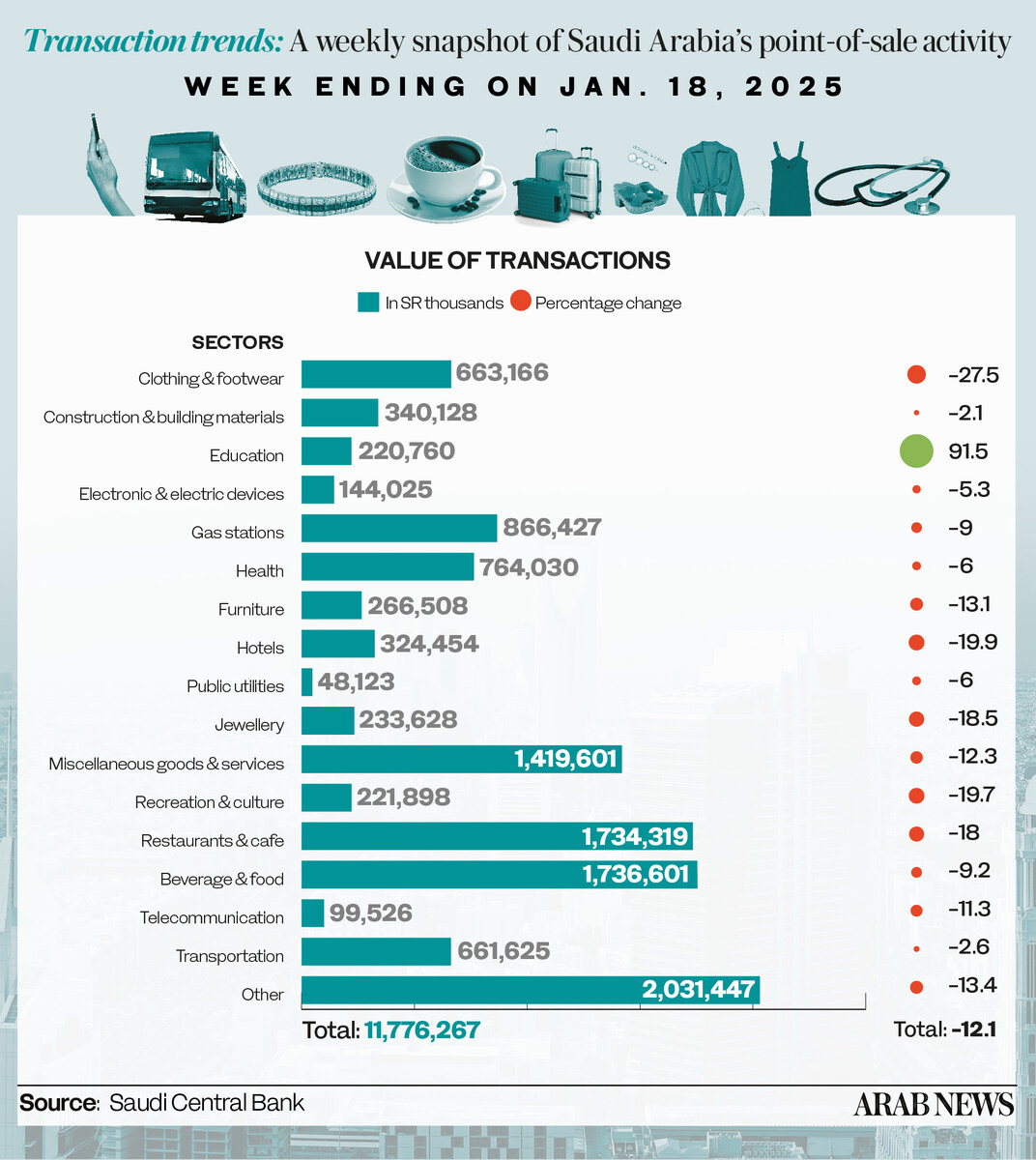

RIYADH: Education spending in Saudi Arabia surged by 91.5 percent to SR220.76 million ($58.8 million) between Jan. 12 and 18, fueled by students returning to school after the midyear break.

According to the latest point-of-sale transactions bulletin, this sector was the only one to register positive growth during the week, with the number of transactions rising by 60 percent to 153,000.

The education sector experienced a 44.4 percent drop in transaction value to SR115.2 million from Jan. 5 to 11, before rebounding this week.

Overall POS transactions in Saudi Arabia declined by 12.1 percent, dropping to SR11.77 billion from SR13.4 billion the previous week, as spending in other sectors cooled, revealed the bulletin issued by the Saudi Central Bank.

Spending on clothing and footwear saw the sharpest decline, falling 27.5 percent to SR663.16 million. Expenditure on hotels followed with a 19.9 percent dip to SR324.45 million, while recreation and culture recorded a 19.7 percent drop to SR221.8 million.

Spending on food and beverages recorded a decrease of 9.2 percent to SR1.73 billion, claiming the biggest share of the total POS value. Expenditure in restaurants and cafes followed, recording an 18 percent decrease to SR1.73 billion.

Miscellaneous goods and services accounted for the third biggest POS share with a 12.3 percent downstick, reaching SR1.42 billion.

Spending in the leading three categories accounted for approximately 41.5 percent or SR4.8 billion of the week’s total value.

At 2.1 percent, the smallest decrease occurred in spending on construction materials, leading total payments to reach SR340.1 million.

Expenditures on transportation followed dipping by 2.6 percent to SR661.6 million, while public utilities recorded a 6 percent fall to SR48.1 million.

Geographically, Riyadh dominated POS transactions, representing around 35.5 percent of the total, with expenses in the capital reaching SR4.18 billion — a 9 percent decrease from the previous week.

Jeddah followed with a 12.5 percent dip to SR1.71 billion, and Dammam came in third at SR602.91 million, down 7.1 percent.

Madinah experienced the most significant decrease in spending, dipping by 19.6 percent to SR471 million.

Hail and Makkah followed recording decreases of 18.6 percent and 17 percent reaching SR171.87 million and SR497.28 million, respectively.

Madinah and Makkah saw the largest decreases in terms of number of transactions, slipping 13.5 percent and 12.7 percent, respectively, to 7.98 million and 8.18 million transactions.

The Kingdom’s POS transactions saw a decline in the week from Jan. 5 to 11, with the total number of transactions dropping by 3.7 percent to 216.5 million. The value of transactions fell by 11.2 percent to SR13.4 billion.

Key sectors experienced significant contractions, including telecommunications at 20.4 percent and transportation at 20.9 percent. The downturn in spending was also evident in discretionary sectors like clothing and footwear, which saw an 18.7 percent drop in transaction value.

The hotel sector was the only industry to show growth, with a 12.5 percent rise in the number of transactions and a 1.1 percent increase in transaction value.

Riyadh and Jeddah, the two largest markets, saw transaction values decline by 10 percent and 7.8 percent, respectively, signaling a broader slowdown across major cities.