DUBAI: The UAE and Egypt appear the most attractive among major Middle Eastern stock markets in an era of low oil prices, the latest Reuters survey of regional asset managers suggests.

The plunge of oil and equity prices over the last several months has stunned managers, and they may therefore invest their 2015 equity allocations to the region only gradually.

“I think the next three months will witness a wait-and-see approach by most fund managers, as they wait to see stability in the equity markets after the wild swings of December,” said Mohammed Ali Yasin, managing director at Abu Dhabi’s NBAD Securities.

A key question, he said, is “if the predictions of more stable oil prices in the range of $65-$75 materialize — that will be a major defining factor for their investment strategy over the rest of 2015.”

However, the Reuters survey of 15 leading Middle East investment professionals, conducted over the past 10 days, shows the markets’ tumble has not turned funds away from regional stocks in general.

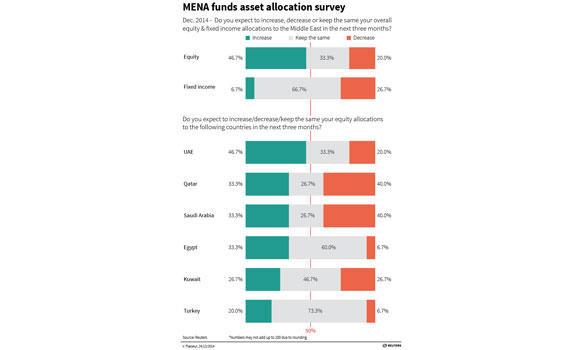

Forty-seven percent expect to raise overall equity allocations in the next three months against 20 percent who anticipate reducing them.

Many fund managers note that the markets’ slide — Saudi Arabia is down 24 percent from its September peak — has greatly improved valuations, reducing or eliminating big premiums to other emerging markets.

The big difference shown by the latest survey is that funds have become much more selective about which stock markets they plan to buy in coming months. On balance they are still wary of Saudi Arabia, for example; 40 percent expect to lower their equity allocations there and 33 percent to increase them.

That is because petrochemical stocks are heavily weighted in the Saudi market and they remain vulnerable to further falls in oil prices, which would reduce the advantage that Saudi companies enjoy over foreign rivals due to cheap feedstock.

“With oil prices expected to remain low and the petchem sector weight big in the index, next year will be very interesting when it comes to stock picking,î said Bader Al-Ghanim, head of asset management at Kuwait’s Global Investment House.

Fund managers are also cautious about Qatar, where petrochemical firms such as Industries Qatar IQCD.QA are heavily weighted, and Kuwait, which has one of the richest governments in the region but where bureaucracy and political tensions have made it hard for authorities to spend money effectively to offset poor global economic conditions.

But toward the UAE and Egypt, managers are considerably more optimistic. Forty-seven percent expect to raise overall equity allocations to the UAE in the next three months and 20 percent anticipate reducing them.

There are two major reasons. Partly because of the contribution of Dubai, economic growth depends less on oil in the UAE than it does in the other wealthy Gulf states.

Also, oil and petrochemical firms are weighted only lightly in the Abu Dhabi and Dubai stock markets, which are instead dominated by banks and real estate firms. If cheap oil strengthens the global economy, that could conceivably help Dubai real estate stocks by increasing the amount of money flowing into Dubai property from India, Europe and elsewhere.

Egypt looks like the other big beneficiary of cheap oil, since it is a net energy importer. Low oil prices might cause Gulf governments to become a little less generous in their foreign aid to Egypt — but not enough to offset the major benefit to its external balance and state finances.

A third of managers expect to raise their Egyptian equity allocations and only 7 percent to reduce them.

Turkey may also benefit from cheap oil, though that is partly offset by worries about capital outflows from emerging markets due to expected rises in US interest rates next year. Twenty percent of fund managers expect to raise their equity allocations to Turkey, and only 7 percent to cut them.

![]()

![]()

Asset managers positive on UAE, Egypt stocks

Asset managers positive on UAE, Egypt stocks

Latest updates

Recommended

© 2026 SAUDI RESEARCH & PUBLISHING COMPANY, All Rights Reserved And subject to Terms of Use Agreement.