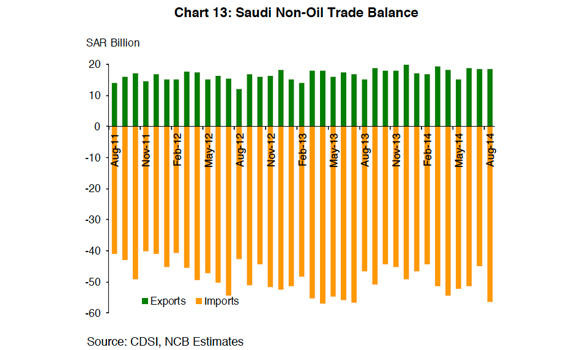

Saudi exports continued their consistent annualized growth in August after realizing SR18.5 billion in returns, a 22 percent surge over the same period last year. Monthly volatility noticeably dampened this year, averaging at around SR18.2 billion a month. The contractual nature of most of the Kingdom’s heavyweight exports limited the negative spillover effects from the waning global demand. Imports, on the other hand, recorded SR56.5 billion; a 19.6 percent Y/Y expansion, according to a report by the National Commercial Bank (NCB).

The data decoupled from last year’s trend in July after it recorded the largest slump to date with SR46.4 billion. This anomaly, along with August’s double-digit growth, occurred in correlation with the shifting seasonality of Ramadan leading to higher annualized data dispersion in July and August. Therefore, the balance of trade gap has widened by 18.4 percent in August compared to last year.

In value terms, the NCB report said more than 34 percent of the export composition consisted of plastics, valued at around SR6.3 billion, and thus leaping over last year’s figure by 7.8 percent. Chemical products recorded SR5.4 billion, rising by 4.4 percent Y/ Y, and making up 29.5 percent of the exports revenue.

Exports of base metals were valued at SR1.7 billion, a solid annualized surge of 42.1 percent despite sliding commodity prices. By destination, the UAE received the lion’s share of just under SR2 billion worth of exports, thus surging by 44.5 percent Y/Y. China came in as a close second with SR1.87 billion, a figure 14.9 percent lower than last year’s, indicating that Chinese troubles are taking their toll on the country’s insatiable demand. India rose above Singapore as the third largest trading partner in August attracting exports valued at SR1.1 billion, a soaring 38.8 percent Y/Y upturn. Machinery and electrical equipment continue to dominate as the most sought after imports in the Kingdom, allocating almost 28 percent of the monthly import bill for this category.

In the month of August, imports of machinery and electrical equipment surged by around 25 percent compared to last year, recording SR15.7 billion. This surge stems from the government’s continued expansionary fiscal policy which includes a 25 percent increased spending on infrastructure projects such as railways, roads and airports. Construction companies raised their capital expenditure to cope with the scope of these projects which also reflected on imports of transport equipment, surging by 28.6 percent to SR9.7 billion.

Imports of base metals also posted a double-digit growth of 21.7 percent worth SR6.9 billion. Over 15.4 percent of the import bill came from China which at SR8.7 billion rose by 35.4 percent Y/Y. US imports to the Kingdom also saw a double-digit growth of 12.7 percent versus last year, valued at SR7.1 billion. Germany is the third largest source of imports as it accounts for over 7 percent of the import bill at SR4 billion.

The NCB report said settled letters of credit (LCs) in the month of August totaled SR20.8 billion, marking the first pick-up since May. On an annual basis, LCs surged by 80.7 percent due to a relatively low figure in August 2013 of just SR11.5 billion. LCs of motor vehicles retained their share as the largest category of goods financed through banks, posting SR4.3 billion, which also returned it to positive annual growth territory of 38.4%. Machinery LCs recorded SR2.2 billion, a staggering 104 percent upturn compared to last year. Building materials’ LCs also soared 80.5 percent Y/ Y, recording SR2.1 billion.

![]()

Saudi imports rise 19.6 percent to SR56.5 billion

Saudi imports rise 19.6 percent to SR56.5 billion

Latest updates

© 2026 SAUDI RESEARCH & PUBLISHING COMPANY, All Rights Reserved And subject to Terms of Use Agreement.