RIYADH: Saudi Arabia’s Industrial Production Index increased by 20.8 percent from a year ago, according to the General Authority for Statistics.

The Saudi IPI saw an extensive period of negative growth rates in 2019 and 2020, which was in part an effect of the global pandemic, showed the GASTAT report.

In May 2021 the IPI growth flipped to positive and has been accelerating from January through April this year to record a high of 26.7 percent year-on-year.

Growth slowed to 24 percent in May and a further 20.8 percent in June.

“The IPI continued to show positive growth rates due to the high production in mining and quarrying, and manufacturing activity,” GASTAT said.

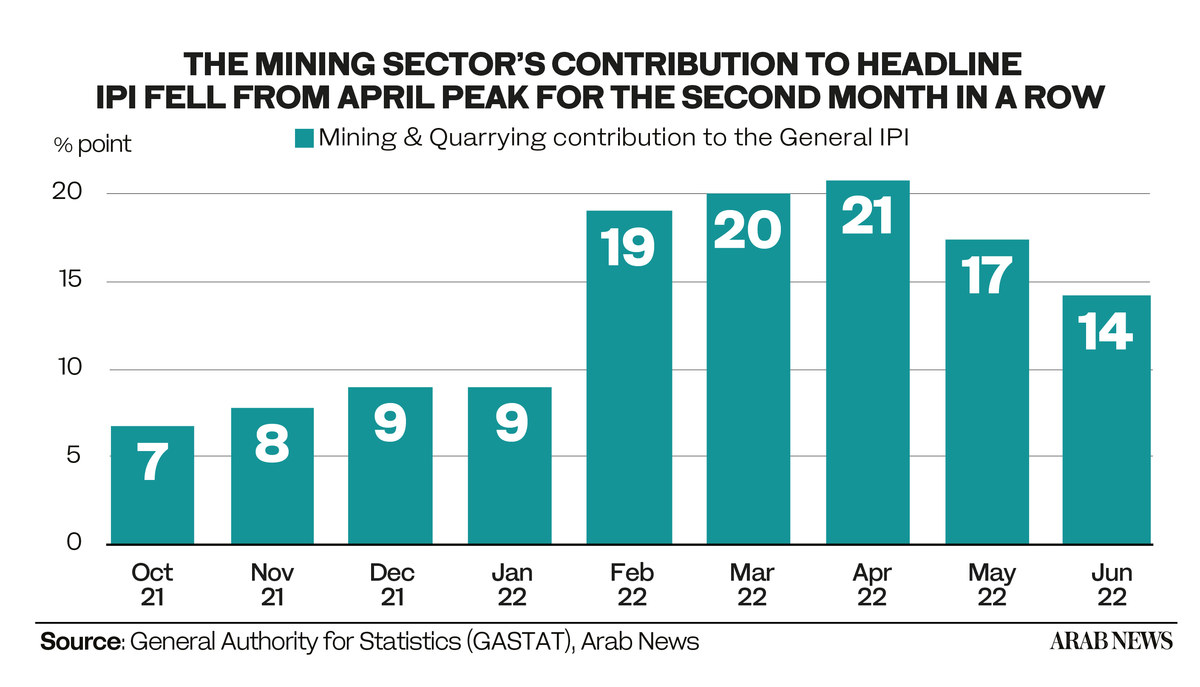

The weight of the mining and quarrying sector alone stood at 74.5 percent, showing a dominating effect on the IPI.

“In June 2022 mining and quarrying grew by 19.2 percent compared to June 2021 as Saudi Arabia increased its oil production to its highest level by more than 10 million barrels per day in June 2022,” stated the GASTAT report.

The annual growth in mining and quarrying index has slowed for the second consecutive month from April when it peaked at 28.3 percent, according to data compiled by Arab News.

Although mining and quarrying is the main contributor to the headline IPI with a weight of almost three-thirds, its share contribution declined by almost 7 percentage points compared to April.

The rate of annual growth in manufacturing has been accelerating for the past eight months from 4 percent to 29.3 percent in June, the highest on record, GASTAT data showed.

Given its 22.6 weight in the general index, its share contribution increased by almost a full percentage point in June compared to April.

When compared to October 2021, the increase recorded was almost 6 percentage points, showed the report.