What happened:

Austria and Denmark have announced measures to gradually reopen economic activity and schools, while keeping some restrictions in place, particularly for the at-risk groups of the population.

France, Spain, Belgium and Finland are also discussing plans on restarting their economies. In other European countries, rifts among political parties have emerged on how long to keep their economies shut down.

This is the backdrop against which the Eurozone finance ministers are holding a virtual meeting to discuss a rescue package potentially surpassing $500 billion. Individual countries have so far provided fiscal stimulus of up to 3 percent and liquidity guarantees up to 18 percent of their GDPs.

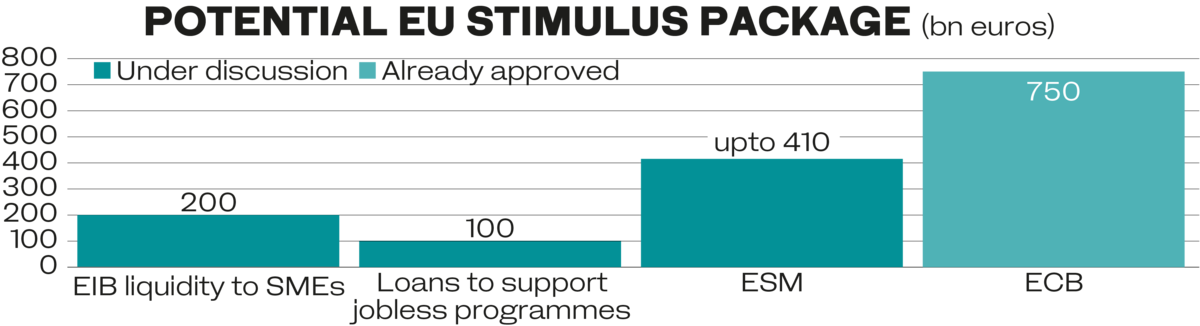

The focus of today’s meeting will be Eurozone measures. Under discussion will be using part of the European Stability Fund (with a remaining debt capacity of €410 billion), a €100-billion program for jobless schemes, and a €200-billion facility to provide liquidity to small- and medium-sized enterprises.

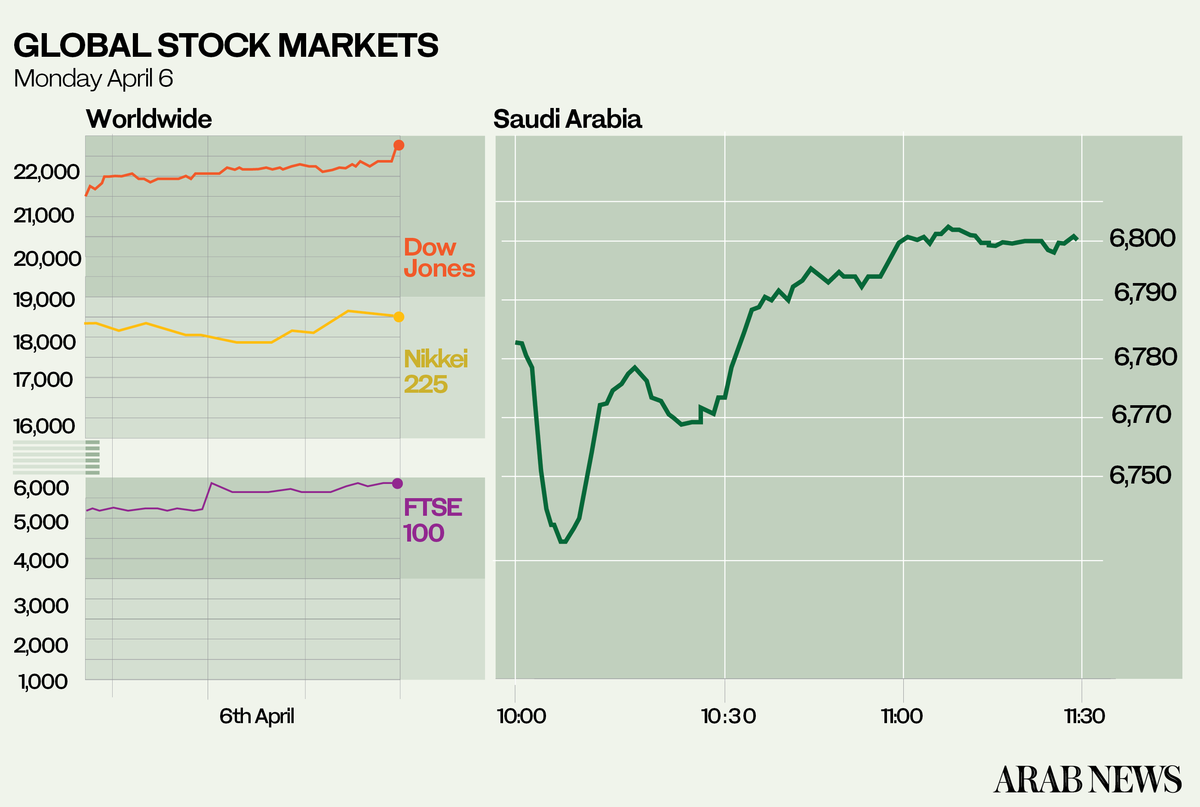

On Monday the Dow Jones jumped 7.7 percent on hopes that the coronavirus disease (COVID-19) outbreak was showing signs of slowing in major economies, and the gains continued into Asia with the Nikkei up 2 percent and the MSI Asia up more than 2 percent on the back of a nearly 3 percent rise on Monday. The STOXX 600 was up by 3 percent in early European trade, and US futures rose too.

Oil was also rising markedly on hopes that a virtual meeting of OPEC+ countries on Thursday will result in substantial production cuts and an end to the Saudi-Russian battle for market share.

Why it happened:

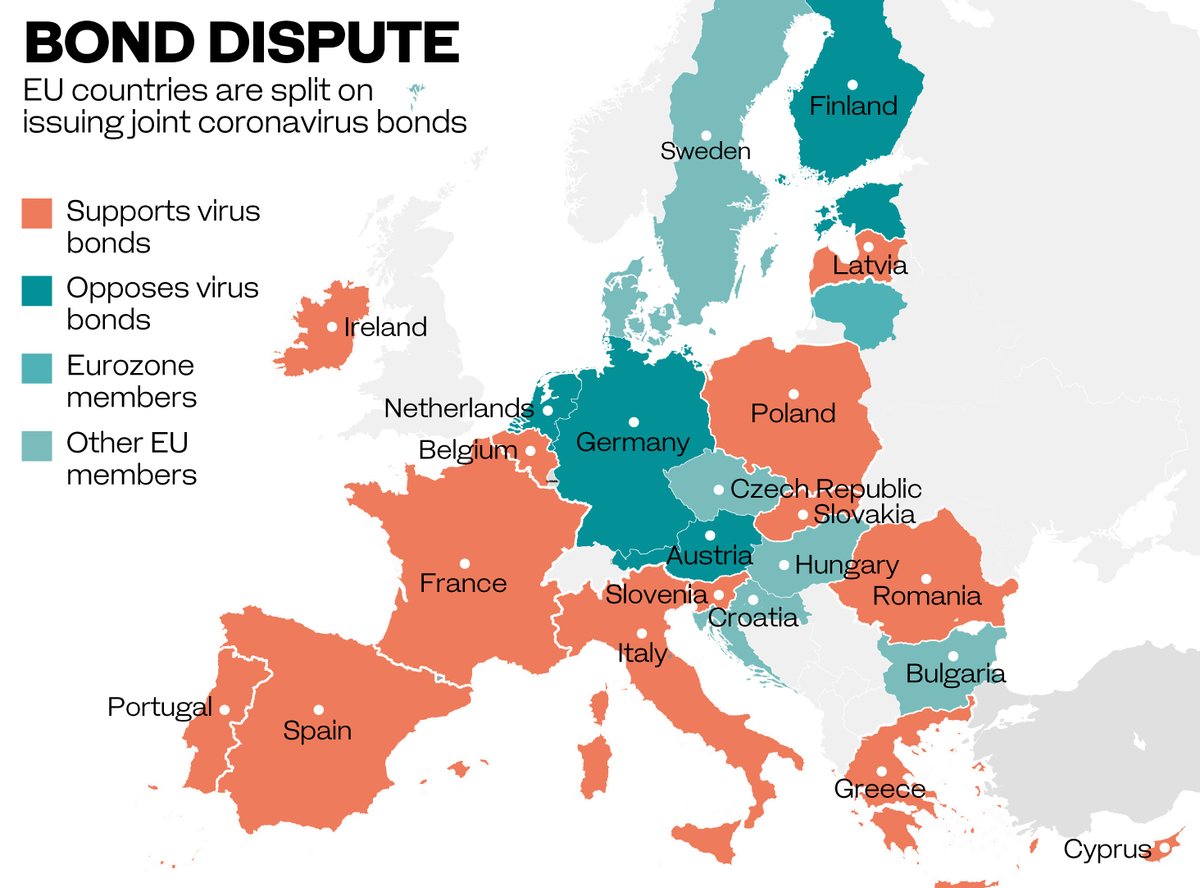

Eurozone finance ministers’ meeting: Hardest-hit Italy, France and Spain ask for coronabonds, which would be issued on a joint basis by all member states. Germany, Holland, Austria and some other northern states oppose a common issuance of debt for fear that they would be on the hook for debt to the highly indebted southern periphery of the eurozone indefinitely. They prefer the ESM (European Stability Mechanism) instead, which allows countries to borrow on their books.

To be fair, finding a solution acceptable to all is not easy in the eurozone. For one there are the Maastricht criteria, which stipulate that budget deficits must not exceed 3 percent and that total government debt must not be more than 60 percent of GDP, which most countries do not meet.

The euro is also a single currency spanning 19 countries with 19 different fiscal regimes, which makes crisis management difficult to say the least.

The northern European states have been criticized for their opposition to common debt in the face of a crisis. The main question is what to do with Italy once the COVID-19 crisis subsides. By then the total government debt to GDP may well exceed 150 percent of GDP.

In a show of solidarity German Chancellor Angela Merkel said on Monday that “more Europe, a stronger Europe and a functioning Europe was needed” to overcome the crisis. Her government still opposes any form of common pooling of debt.

Where we go from here:

It might be overly optimistic to interpret at the current stock market gains that the market has found its level. J. P. Morgan’s chief Jamie Dimon warned that the COVID-19 crisis should be compared to the 2008 financial crisis. Veteran investor and market watcher Tom Barrack of Colony Capital was even more bleak in his outlook.

The OPEC+ meeting will in all probability find a compromise, if for no other reason than that the world is running out of storage space for both crude and products. There is a possibility of a G20 virtual meeting of energy ministers, which could provide an opening for Mexico, Brazil and Canada to join in. Norway is also said to be looking at participating in a global reduction of output.

Speaker of the US House of Representatives Nancy Pelosi is asking for an additional rescue package of $1 trillion.

— Cornelia Meyer is a Ph.D.-level economist with 30 years of experience in investment banking and industry. She is chairman and CEO of business consultancy Meyer Resources.Twitter: @MeyerResources