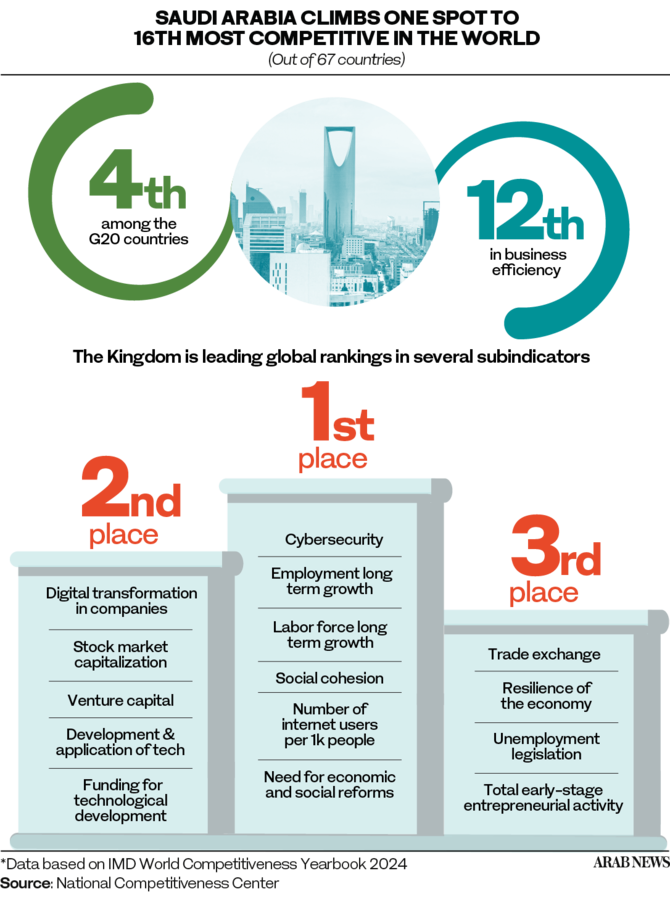

RIYADH: Saudi Arabia’s ongoing economic diversification efforts have propelled the country to the 16th spot in the World Competitiveness Index 2024, up one place from the previous year.

According to a report from the Switzerland-based International Institute for Management Development, the Kingdom was ranked 24th in 2022 and 32nd in 2021.

The ascent, supported by Saudi Arabia’s Vision 2030 program, is attributed to significant progress in economic performance, government efficiency, and a business-friendly environment.

The report also highlighted that Saudi Arabia ranked higher than several of its G20 peers, including India, the UK, and Japan, as well as other countries like Italy, Argentina, Indonesia, and Brazil and Turkiye.

Majid bin Abdullah Al-Qasabi, Saudi Arabia’s minister of commerce, said that the nation’s growth in the ranking is a testament to the Kingdom’s ongoing economic transformation process, which is being implemented in accordance with the directives of Crown Prince Mohammed bin Salman, according to a press statement.

Saudi Arabia leading several subindicators in the ranking

The Kingdom also grabbed top spots in several subindicators in the ranking, garnering the first position in cybersecurity and long-term employment growth.

Saudi Arabia was also ranked first in other subindicators, including long-term labor market growth and the number of internet users per thousand people.

The report revealed that the Kingdom was ranked 12th in business efficiency globally, while it secured second place in stock market capitalization and digital transformation implemented in companies.

Saudi Arabia was also ranked second in indicators such as the availability of venture capital, the development and application of technology, and the availability of financing in technical development.

Similarly, the nation was ranked third in total early-stage entrepreneurial activity and unemployment legislation.

The Kingdom also grabbed the 34th spot in the list for infrastructure growth, unchanged from the previous two years. In 2020 and 2021, the country’s ranking in this subsection was 36.

However, in terms of economic performance, Saudi Arabia slipped to the 15th spot, down from the sixth position in the previous year but much higher than the 31st and 48th place it procured in 2022 and 2021, respectively.

When it comes to challenges facing the Kingdom, the report flagged up the need to continue efforts to promote renewable energy and reduce carbon emissions.

It also highlighted how Saudi Arabia must keep enhancing its business environment to increase the private sector’s economic participation, as well as continuing to invest in human capital development across all sectors.

Singapore leads the list

Singapore secured first place in the World Competitiveness Index 2024, climbing three spots from the previous year.

“The data shows a particularly robust performance for the island nation (Singapore) across the areas of government efficiency and business efficiency,” said the report.

It added: “In the case of Singapore, potential headwinds to maintaining its position include seizing opportunities and managing disruptions from new technologies, such as AI, by supporting workers in reskilling and businesses in transformation.”

The release further pointed out that Singapore’s small size and maritime setting have also helped it to top the list.

Arturo Bris, director of the IMD World Competitiveness Center, said that the ranking, which is published annually, will help nations achieve their economic goals and ensure sustainability.

“It serves as a benchmark for these countries to measure their progress and identify areas for improvement, offering a clear path toward their economic development but also supporting global goals such as the social development goals,” said Bris.

He added: “The best-performing economies balance productivity and prosperity, meaning they can generate elevated levels of income and quality of life for their citizens while preserving the environment and social cohesion.”

Singapore was followed by Switzerland and Denmark in the second and third spots, respectively.

Ireland was ranked fourth on the list, while Hong Kong and Sweden grabbed the fifth and sixth spots, respectively.

Climbing three positions compared to 2023, the UAE came in seventh place, followed by Taiwan and the Netherlands in eighth and ninth, respectively.

On the other hand, Norway climbed four spots from the previous year to 10th place, while Qatar improved its ranking from 12th to 11th this year.

The US, however, slipped by three positions from 2023 to secure the13th rank, followed by Australia, China, and Finland in the next three spots.

Bahrain was ranked 21st on the list from the Middle East region, while Kuwait secured the 37th spot.

The promises and challenges offered by artificial intelligence

According to the report, the widespread adoption of AI seems like a honey pot to economies seeking productivity boosts.

“At the micro level, the recent surge in AI-based technologies could boost efficiency and productivity significantly,” said World Competitiveness Center Senior Economist Jose Caballero.

He further noted that the rise of AI is also posing significant challenges, with several companies seeming less proficient in implementing this advanced technology.

“One of the key challenges for companies is how to implement AI systems that improve efficiency without disrupting business activities. Another is ensuring a chosen AI system’s accuracy; inaccurate systems lead to inefficiencies and reduced productivity,” said Caballero.

He added: “Furthermore, there is a cost-related challenge given that initial investments in AI technology can be substantial while the ongoing costs of maintenance and upgrades to the systems can be significant.”

The study further pointed out that AI is the top concern for executives from Western Europe, Western Asia and Africa, and Central Asia, as well as, Southern Asia and the Pacific, North America, and South America.

On the other hand, executives from Eastern Asia and Eastern Europe are most concerned about a global recession, while most participants across the board deprioritize environmental risks.

“With executives under pressure to balance short-term and long-term priorities, environmental risks are being pushed to the back of the queue,” said the report.