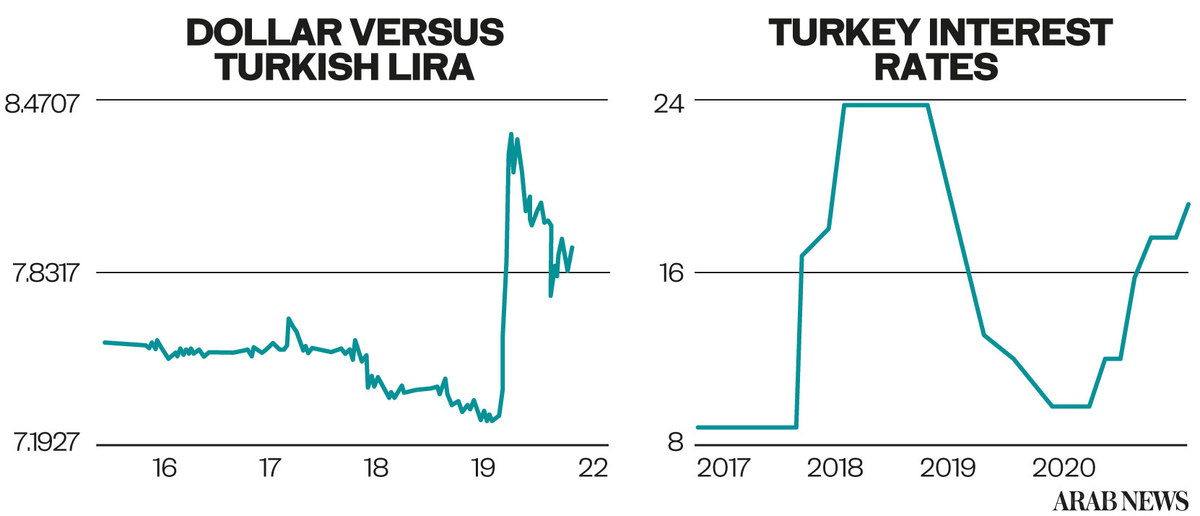

DUBAI: The Turkish lira crashed by nearly 15 percent Monday after the sacking of the country’s central bank chief rattled global markets.

The currency fell to as low as 8.47 against the dollar compared to 7.22 on Friday.

The currency recovered slightly later in the session to 8.09.

President Recep Tayyip Erdogan's abrupt dismissal of the reformist governor Naci Agbal sent shock waves across markets and triggered fresh worries for millions of Turks concerned about their savings.

The governor was replaced by former ruling party lawmaker Sahap Kavcioglu over the weekend.

A presidential decree on Friday did not explain why Agbal had been removed, but it comes a day after the bank hiked interest rates more than two percentage points to 19 percent in a bid to fight inflation.

“We now see the possibility of an inter-meeting interest rate cut under the new governor, alongside the potential for accelerated capital outflows,” said Abu Dhabi Commercial Bank chief economist Monica Malik, in a note to investors on Monday.

The Borsa Istanbul suspended trading twice when automatic circuit breakers kicked in amid a huge sell-off nearing 8 percent.

Yields on Turkish bonds also rose to record highs.

The fallout was felt across global currency and equities markets. The dollar gained as investors sought safety in the greenback while at the same time some companies with exposure to Ankara had their share price hammered.

Shares in Spain’s BBVA, which makes around 14 percent of its profits in Turkey through its Turkish unit Garanti, plunged as much as 7.7 percent.

The MSCI emerging market currency index was down about 0.1 percent, with high-yielding currencies including the South African rand and the Mexican peso easing about 0.8 percent and 1.4 percent, respectively.

“It may well be that interest rate hikes are once again permitted by Erdogan in a phase of crisis-like lira depreciation but the recent developments should have shown currency traders that even then a sustainable monetary policy regime change is not to be expected,” said Ulrich Leuchtmann, head of FX at Commerzbank.

“The calming effect of interest rate hikes has probably been largely destroyed.”

(With agencies)