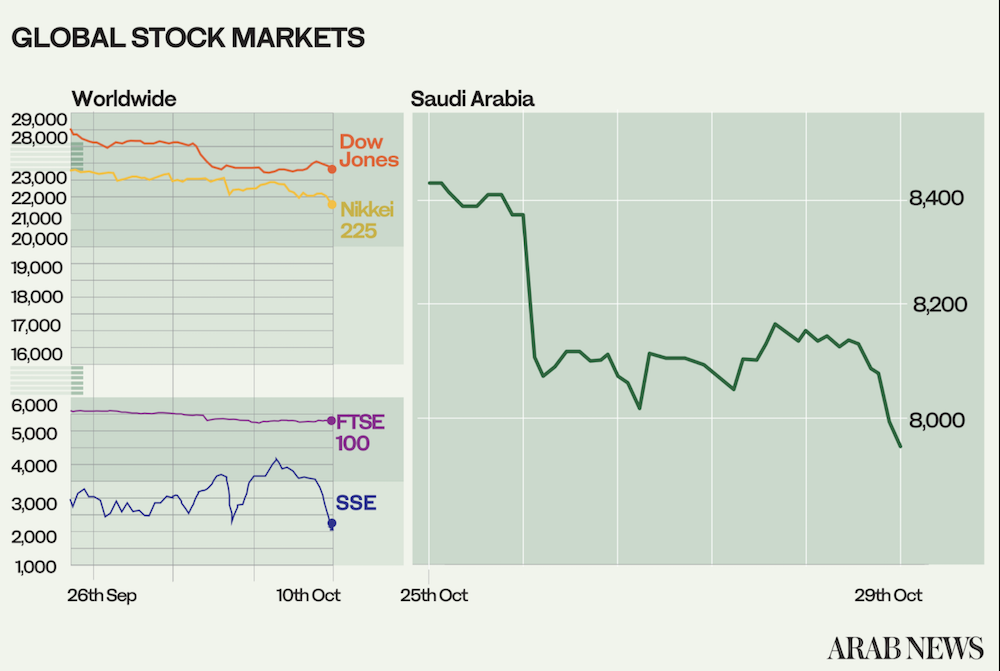

The Week That Was: Market sentiment was markedly risk off as COVID-19 cases surged in the northern hemisphere, surpassing 45 million globally. This was one of the most difficult weeks for equity markets since March.

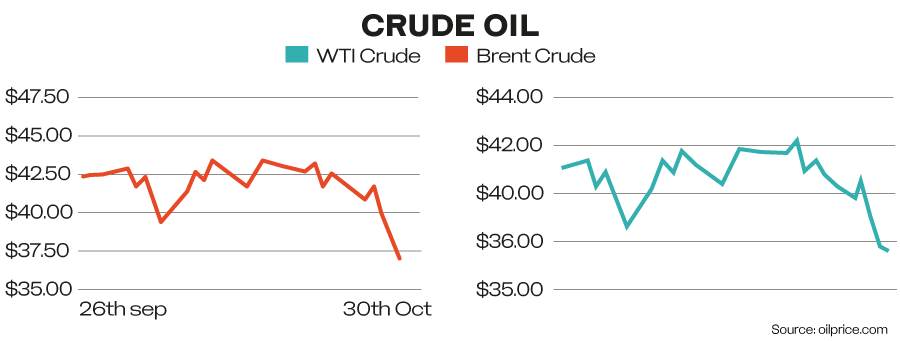

Oil dropped below $40 per barrel, with both WTI and Brent trading around the mid-$30 range over demand concerns due to restrictions and lockdowns.

There is a huge inventory overhang which depends on consumption in order to decline. At the same time, incremental barrels are hitting the market, particularly from Libya, where production might reach 1 million barrels before the end of the year. OPEC may consider whether to extend the 7.7 million barrel per day production cuts into 2021.

Third quarter gross domestic product numbers for the US and euro zone beat expectations by and large. The US came in +33.1 percent compared to the previous quarter (-31.1 percent). The euro zone came in at +12.7 percent according to Eurostat, with Germany +8.3 percent (-10 percent in 2Q), France +18.2 percent (-13.7 percent in 2Q), and Italy +16.7 percent (-13 percent in 2Q).

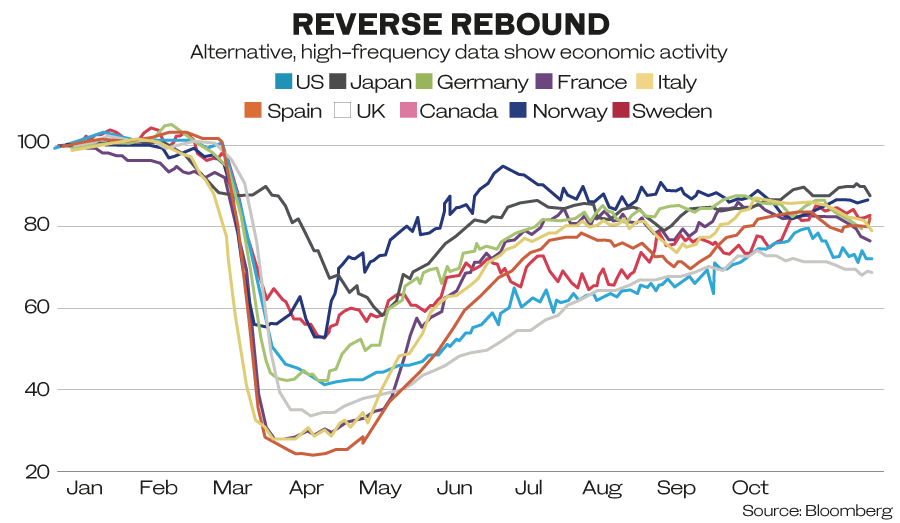

These numbers reflect the past. The future is one of further restrictions of economic activity and lockdowns.

Economic activity across the northern hemisphere slowed. This will be most pronounced in Europe as country after country restricts economic activity. Some, like France, have even entered into full-scale lockdowns again. North America will also see a slowdown as virus cases surge.

The European Central Bank held rates steady. President Christine Lagarde expects further stimulus, which probably means expanding the Pandemic Emergency Purchasing Programme (PEPP), which stands at €1.35 trillion ($1.75 trillion).

There may be less flexibility on interest rates, because a return to profitability is the biggest concern for the banking sector. Commercial and retail banking operations depend on interest rates to improve profitability. Lagarde reminded politicians that fiscal stimulus was key in dealing with the economic downturn.

The Bank of Japan (BOJ) also kept interest rates stable. Gov. Haruhiko Kuroda said that the BOJ did have capacity for further stimulus, but like Lagarde, he focused on the need for fiscal stimulus.

Going forward, the Japanese economy will need to find new drivers for growth after the pre-Olympic construction boom closed. This will most likely come from digitalization where the country is lagging.

The earnings season continues with big oil and big tech reporting.

Shell rallied 5.1 percent on announcing it would increase its dividend by 4 percent to 16.65 cents a share and expected to continue on a similar trajectory going forward. The company also expects to reduce the number of refineries to six over the coming years. Adjusted earnings beat expectations with $955 million for Q3 compared to $4.77 million during the same quarter in 2019. Compared to January the share price is down 61 percent.

Total’s results were well received. Net income was $850 million down 72 percent compared to the same quarter last year. EPS was 29 cents down 74 percent. The company said it was comfortable with an oil price at $40 and produced a positive cashflow of around $44 billion. According to management, the company can break even on a cash basis with an oil price of $25, which seems ambitious.

BP returned to profitability with a net profit of $100 million compared to a loss of $6.7 billion for the second quarter. Earnings after tax stood at $271 million. Dividend per share is 5.25 cents.

Equinor disappointed with a 3Q loss of $2.12 billion. The results were impacted by impairment charges of $2.93, which were based on a reduction of future price assumptions.

In the US, Exxon generated revenues of $46.2 billion and posted a loss of $680 million. The company will let go of 15 percent of its workforce. Chevron’s revenue came in at $24.45 billion and the company posted a loss of $207 million.

SABIC reported a profit of SR1.09 billion ($290.6 million) up 32 percent compared to the same quarter last year, in part owing to the reversal of SR690 worth of impairments for Clariant AG, where SABIC owns a 31.5 percent stake. Revenues fell by 11 percent to SR29.3 billion.

Focus:

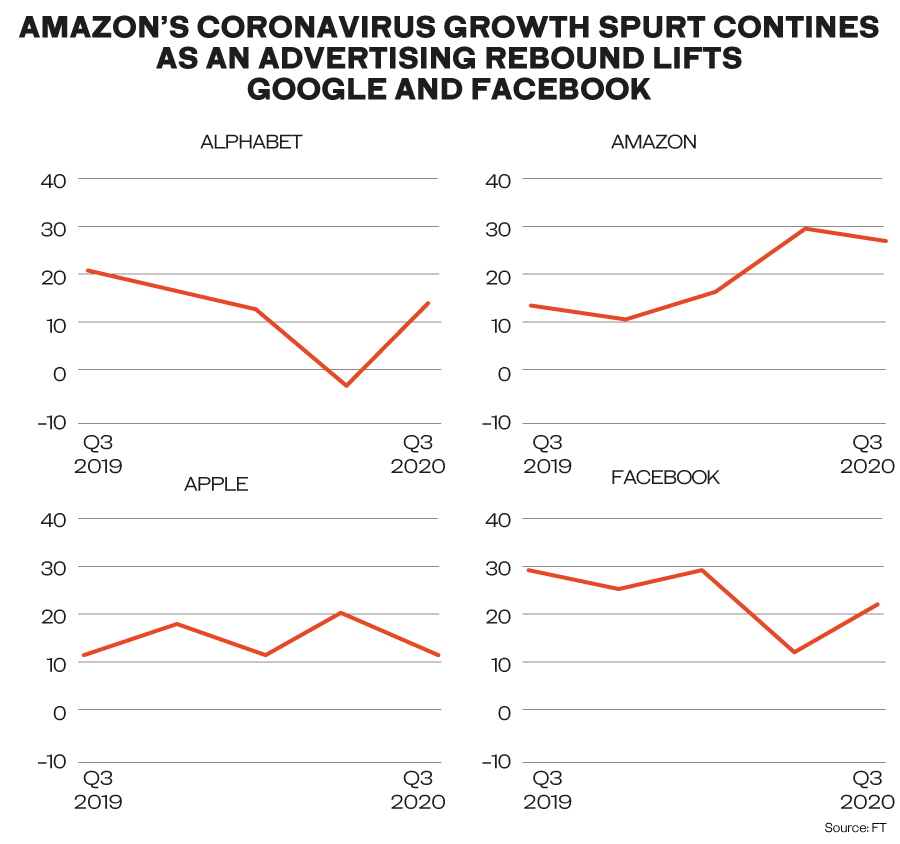

Big tech reported a strong set of earnings which, except for Google parent Alphabet, could not convince investors.

The tech rout started on Wednesday after a bruising testimony by the CEOs of Google, Facebook and Twitter in the US Congress. At issue was Section 230, a 1996 law exempting tech companies from liability over published content – a particularly explosive topic in an election year.

Last week the Trump administration filed an antitrust case against Google, which brought to the fore again that the concentration of tech companies did not sit well with legislators on both sides of the Atlantic.

The European Commission will continue to watch the sector with an eagle eye and more regulation may also be on its way in the US, irrespective of who wins November’s election.

A further explanation for this week’s slump is that tech have been the main winners of the stock market rebound since March, because the products of the FAANGs (Facebook, Amazon, Apple, Netflix and Google) were in particular demand in the face of the pandemic and its lockdowns. This led to a concentration in these stock valuations, resulting in some investors taking profits and rotating out of the sector – particularly if they were spooked by the regulatory outlook (Apple alone constitutes 18 percent of the NASDAQ).

On turning profitable again, Google’s stock rose 9.1 percent. Revenue came in at $46.17 billion, beating expectation by $3.27 billion. EPS was $16.4, beating expectations by 45 percent. YouTube ads and Google Cloud were the star performers.

Apple, Amazon and Facebook beat expectations but their share price still fell. Investors might have preferred to see clearer guidance, which was lacking.

Apple revenue suffered from the delayed release of the latest iPhone model, Amazon invested heavily in its execution capabilities in light of rising demand and Facebook’s month-on-month user numbers were flat. The growth potential for Facebook lies in enhancing the platform for other purposes, such as payment options.

On the other side of the Pacific, investor interest for the Ant IPO measured an enormous $3 trillion. Demand for the retail portion in Shanghai exceeded initial supply by more than 870 times.

The Central Committee of the Communist party in China focused the next five-year plan (2021-2025) on self-reliance in the technology sector. Microchips were of particular interest because the Chinese government no longer believes in its ability to source the product internationally on the free market, which is a legacy of the national security controversy over Huawei.

Where we go from here:

If the outcome of next week’s presidential election in the US is clear, we may get an indication of how economic policy will unfold and what the size of a future stimulus package will be.

All eyes are on the UK, where further lockdown measures may become necessary as the virus spreads.