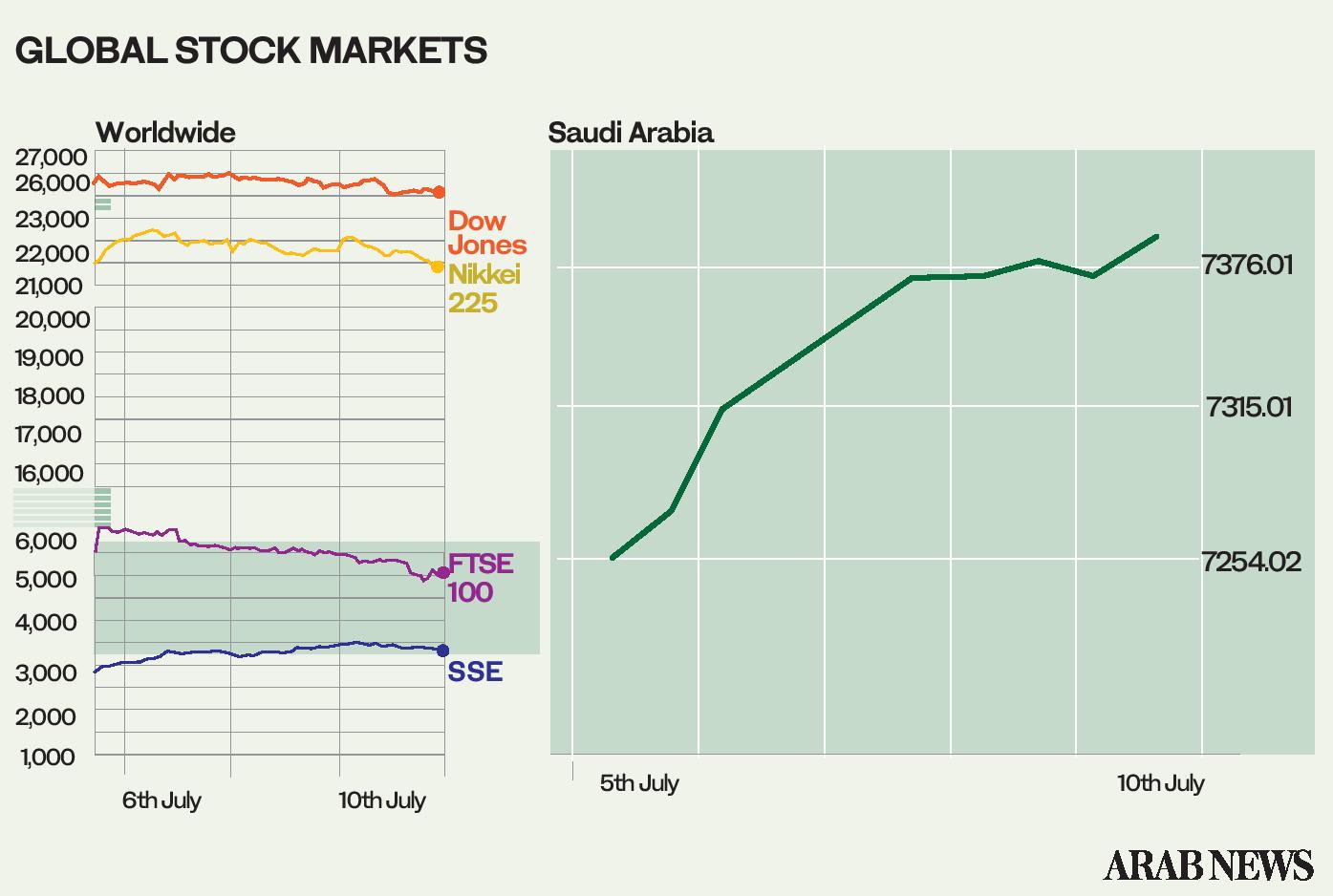

The week that was:

At the beginning of the week global stock markets shrugged off increasing COVID-19 cases in the US amid fears of a second wave in Asia and Australia. As the US surpassed 60,000 new cases the S&P 500 started to fall on Thursday. Asian stocks, including the Shanghai Composite, carried over the losses into Friday. Approaching the weekend, optimism seems to have given way to de-risking.

As COVID-19 cases spiked in the sunbelt, New York, New Jersey and Connecticut increased the number of states requiring incoming travelers to quarantine to 19.

US first-time jobless claims fell to 1.3 million for the week ending July 4, stubbornly remaining above the one million mark

US plans to raise tariffs against France in retaliation for a 3 percent French tax on the in-country revenues of big tech firms, which mainly affects US big tech.

At minus 8.4 percent, the EU predicts the highest drop in gross domestic product (GDP) in the history of the EU. The previous forecast stood at minus 7.4 percent.

UK Chancellor Rishi Sunak unveiled a £30 billion plan to save jobs and the economy. It includes a ceiling on stamp duty for home purchases until March 31, 2021, cutting VAT on restaurants, hotels and attractions by 75 percent for six months and £9 million to protect workers returning from furlough. This sum is in addition to the previous £35 billion to protect the jobs of 12.1 million workers, and the £45 billion for over a million companies under three lending programs.

UK Prime Minister Boris Johnson told German Chancellor Angela Merkel that the UK would exit the EU without a deal if the EU was unwilling to compromise. (Germany assumed the six months rotating presidency of the EU on July 1.) According to UK Environment Secretary George Eustice, it may take until December until an agreement on fisheries can be reached.

Merkel kicked off Germany’s EU presidency with a speech endorsing the EU’s proposed rescue package. It involves the European Commission raising 750 billion euros in debt, constituting a de facto mutualization, much against the wishes of several northern countries. (Consensus is not expected at next week’s summit, but is hoped for before the summer recess).

On Thursday the Eurogroup, consisting of finance ministers from the 19 eurozone countries elected Irish Finance Minister Paschal Donohoe as its president, against the wishes of France, Italy, Spain and Germany, who had supported Spanish Finance Minister María Jesús Montero.

Siemens concluded its restructuring with shareholders approving the spin-off of its energy group comprising coal, gas and wind energy generation. CEO Joe Kaeser announced that the new entity would exit coal at an accelerated pace. The new Siemens consists of three separately listed companies: Siemens Global, comprising industrial automation and digitization, mobility and smart infrastructure; Siemens Healthineers, which was listed in 2018, and Siemens energy, which will be listed at the end of September. Splitting the company up is expected to generate focus and agility.

Background:

COVID-19 has hit the global economy with full force. According to the OECD the G20 GDP contracted by 3.4 percent and is estimated to decline by between 6 and 7.6 percent for the full year, depending on a second wave of COVID-19 outbreaks.

This is the biggest contraction since the Great Depression. It is unsurprising that it led to bankruptcies in the US, which is the world’s largest economy and the worst affected by the virus.

The US has seen a record number of bankruptcies. Retail, travel, leisure and hospitality have been particularly hard hit, but we have also seen energy companies affected, particularly in the shale space with the likes of Chesapeake. Other sectors are also hurting. This will have ramifications on sustained unemployment and consumption down the road. It will also have an impact on the banking sector as many of the insolvent companies are highly levered.

Where we go from here:

The ECB will, in all likelihood, extend its 13.5 billion euros stimulus programs by the end of the year. ECB President Christine Lagarde expects deflation in the eurozone over the next two years. She feels that the economy will need to be supported, because the possibly disruptive shift toward digitization, automation, shorter supply chains and greener industries has been accelerated by the pandemic.

The rally in Chinese stocks seems to have come to a halt for now amid concerns of overheating by Beijing. (The Shanghai Composite has been up by 12 percent this month alone.) This has less of an impact on global equity markets than movements in US exchanges. According to Bloomberg, the effect of the SSE Composite on the MSCI global was less than half compared to the one on the S&P 500 over the last 10 years.

Earnings season in the US will get underway with all of the major US banks reporting next week. The numbers will give us an inkling on how the balance sheets of big banks have been hurt by the downturn and bankcruptcies.

- Cornelia Meyer is a Ph.D.-level economist with 30 years of experience in investment banking and industry. She is chairperson and CEO of business consultancy Meyer Resources. Twitter: @MeyerResources